Financing

Financing

Buying heavy machinery requires serious capital. Whether you operate in construction, agriculture, or industrial manufacturing, acquiring tractors, excavators, or combine harvesters impacts your bottom line heavily. However, smart business owners know that the purchase price is only one part of the financial equation.

Understanding tax codes transforms a massive capital expense into a strategic financial advantage. By leveraging specific tax rules available in 2026, you can significantly lower the effective cost of your machinery. This guide breaks down complex tax regulations into practical strategies, helping you navigate your next heavy machinery purchase with confidence.

Why Tax Strategy Matters When Buying Heavy Equipment

Business growth requires reliable machinery. When you buy a $400,000 John Deere tractor or a Case IH combine, you are not just spending money. You are exchanging cash for an income-producing asset. The US government recognizes this and offers incentives to encourage business investment through tax deductions.

Ignoring tax strategy leaves money on the table. Proper planning reduces your taxable income, which directly lowers your tax bill. Money saved on taxes stays in your bank account, improving cash flow and allowing you to reinvest in your operations.

Timing and structure play massive roles here. Buying a machine in December versus January completely changes your tax liabilities for the year. Similarly, choosing cash over financing alters your immediate cash flow, though both methods offer unique advantages. Securing a proper heavy equipment tax deduction requires aligning your business needs with current tax laws. Tax planning must be an integral step in your equipment sourcing process, not an afterthought left for your accountant at the end of the year.

What Is Section 179 and How Does It Work

Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment bought or financed during the tax year. Instead of writing off the cost little by little over several years, you write off the entire purchase price from your gross income upfront.

One important constraint: your Section 179 deduction cannot exceed your net business taxable income for the year. If your deduction exceeds your income, the excess carries forward to the next tax year – it is not lost, but it does delay the benefit.

Immediate tax relief is the primary goal of Section 179. It was originally designed to encourage business investment across all company sizes. While very large buyers spending over $4,090,000 in qualifying equipment annually will see the deduction phase out dollar-for-dollar, the vast majority of construction, agricultural, and industrial operators fall well below that threshold and qualify for the full deduction. For the 2026 tax year, the deduction limit sits at $2,560,000, with a phase-out that begins only when total qualifying purchases exceed $4,090,000. This means virtually all standard heavy equipment purchases easily qualify for full immediate deduction.

Qualifying equipment includes almost all tangible business property. For agricultural and construction businesses, this covers tractors, loaders, bulldozers, harvesters, and specialized attachments.

Used equipment qualifies just like new equipment for Section 179, provided it is new to your business. For bonus depreciation specifically, used equipment qualifies provided it was both acquired and placed into service after January 19, 2025. Equipment acquired before that date follows the older phase-down rules regardless of when it is put into service, so verify the acquisition date when buying older inventory from dealers or auctions. This makes buying high-quality used machinery from global marketplaces incredibly cost-effective.

Impact on cash flow is immediate and profound. If you buy a machine and deduct its full cost, your taxable income drops by that exact amount. Lower taxable income means a smaller tax check written to the government, keeping vital operating capital inside your business.

What Is MACRS Depreciation

The Modified Accelerated Cost Recovery System serves as the standard depreciation system in the United States. While Section 179 offers an immediate upfront deduction, MACRS spreads the cost of your equipment over its useful life.

Spreading equipment cost over time mimics the actual wear and tear of the machinery. The IRS assigns different property classes to different types of assets. Most heavy construction and agricultural machinery falls into the 5-year or 7-year property class.

The difference from immediate deduction is straightforward. Instead of taking a massive deduction in year one, you take calculated percentages of the equipment cost each year. MACRS uses a declining balance method, meaning you get larger deductions in the early years and smaller deductions in the later years.

Setting up a proper equipment depreciation schedule ensures you capture tax benefits consistently over the lifespan of the machine. This structured write-off helps businesses that might not need a massive tax break today but want steady deductions to offset future income.

You can find official property classes and recovery periods directly through IRS Publication 946, which governs how to depreciate property.

Section 179 vs MACRS: What Is the Difference

Choosing between these two methods depends entirely on your current financial situation and future projections. Both methods save you money, but they deliver those savings on completely different timelines.

Immediate deduction belongs to Section 179. You buy the equipment, put it into service, and deduct the entire cost in that exact same tax year. This generates a massive short-term benefit.

Gradual depreciation belongs to MACRS. You buy the equipment, put it into service, and deduct a specific percentage each year for five to seven years. This generates long-term, steady benefits.

Cash flow impact differs drastically. Section 179 provides a fast cash infusion by slashing your current tax bill. MACRS provides gradual tax relief, keeping your tax bills slightly lower over nearly a decade.

| Feature | Section 179 | MACRS | Bonus Depreciation |

|---|---|---|---|

| Deduction timing | Full deduction in year one | Spread over 5–7 years | Full deduction in year one |

| 2026 deduction limit | $2,560,000 | No dollar cap | No dollar cap |

| Income limitation | Cannot exceed net business income | None | None |

| Can create a net operating loss | No | No | Yes |

Applies to used equipment | Yes, if new to your business | Yes | Yes, if acquired after Jan 19, 2025 |

| Election required | Yes — you must elect it | Default (automatic) | Automatic unless you opt out |

| Best for | High-profit years | Spreading deductions across future high-income years | Any income level; especially low-income years |

| Phase-out threshold | Begins at $4,090,000 | None | None |

| State conformity | Most states conform (with own caps) | All states conform | Many states do not conform |

Comparing the two requires looking at your profit margins. If you had a record-breaking year with massive profits, Section 179 wipes out a large chunk of your tax liability. If you are a new business with slim margins this year but expect massive growth next year, saving your deductions through MACRS makes much more mathematical sense.

Neither option may be optimal in every situation. Bonus depreciation, covered in the next section, adds a third path, one with no income cap and no dollar ceiling, that often works alongside or instead of both, depending on your income level and growth trajectory.

Bonus Depreciation: How It Fits Into the Picture

Bonus depreciation acts as another powerful tool for business owners. It allows you to deduct a significant percentage of the purchase price of eligible assets in the first year they are placed in service.

The additional depreciation option works alongside standard methods. Bonus depreciation was originally scheduled to phase down to 20% in 2026 and disappear entirely by 2027. However, the One Big Beautiful Bill Act, signed into law on July 4, 2025, permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025.

Works as a powerful complement to Section 179. IRS rules require that Section 179 be applied first. If you have already maxed out your Section 179 limit, or if your taxable income is too low to absorb a full Section 179 deduction, bonus depreciation picks up the remainder – potentially allowing you to write off the entire equipment cost in year one through the combination of both provisions.

| Scenario | Business Net Income | Section 179 Applied | Bonus Depreciation Applied | Remaining MACRS Basis | Total Year-One Deduction |

|---|---|---|---|---|---|

| High-income year | $400,000 | $300,000 | $0 | $0 | $300,000 (100%) |

| Low-income year | $50,000 | $50,000 (capped by income) | $250,000 | $0 | $300,000 (100%) |

| Zero-income year | $0 | $0 (no income to absorb) | $300,000 | $0 | $300,000 (100%) – creates $300,000 NOL carry-forward |

| MACRS only (no elections) | Any | $0 | $0 | $300,000 | $60,000 (20% year-one only) |

In every income scenario, the combination of Section 179 and bonus depreciation allows a full year-one write-off of the $300,000 purchase. The key difference is which tool does the heavy lifting. In high-income years, Section 179 handles it entirely. In low or zero-income years, bonus depreciation absorbs what Section 179 cannot – and can generate a net operating loss that reduces taxes in future profitable years.

Carries no income limitation, unlike Section 179. This is a critical distinction. Section 179 cannot exceed your net business income for the year. Bonus depreciation has no such cap, meaning it can generate a net operating loss that carries forward to offset future taxable income. For businesses in a lower-income year purchasing expensive equipment, this makes bonus depreciation an especially powerful tool.

How Much Can You Actually Save

Real tax savings depend directly on your business income, your corporate tax rate, and the cost of the machinery. Tax deductions do not mean the equipment is free. They mean the government subsidizes a portion of your purchase by waiving the taxes you would have paid on that money.

Effective purchase cost calculation shows the real power of these deductions. Let us look at a practical example using a profitable construction firm buying an excavator.

Purchase Details

| Cost Category | Amount |

|---|---|

| Equipment Purchase Price | $300,000 |

| Section 179 Deduction | $300,000 |

| Corporate Tax Bracket | 21% |

| Total Tax Savings | $63,000 |

| Effective Equipment Cost | $237,000 |

Logic dictates that because you deducted $300,000 from your taxable income, you no longer owe the 21% tax on that $300,000. That saves you $63,000 in hard cash. Your $300,000 excavator effectively costs your business $237,000.

Securing a heavy equipment tax deduction requires the equipment to be put into service before December 31 of the tax year. Buying the machine and leaving it in a storage facility does not count. It must be actively ready and available for your business operations.

When Section 179 Makes Most Sense

Certain business scenarios scream for immediate tax relief. Section 179 serves as a financial shield for businesses facing heavy tax burdens.

Profitable businesses benefit the most. If your agricultural operation had an incredible harvest resulting in high taxable net income, your tax bill will be painful. Buying necessary farm equipment and applying Section 179 drops that net income instantly, keeping your hard-earned money out of government hands.

The need for immediate tax reduction drives end-of-year purchases. Many businesses review their financials in November. If profits are unexpectedly high, purchasing a loader or tractor in December becomes a strategic move. You get the equipment you need for the upcoming spring season while erasing a massive chunk of your current year tax liability.

Cash flow advantage cannot be overstated. By reducing your current tax bill, you keep cash liquid inside your business. This liquid cash can cover payroll, emergency repairs, or facility expansions.

When MACRS Is a Better Option

Taking all your deductions up front is not always the smartest move. Sometimes, spreading the tax benefits over several years aligns better with your business trajectory.

Lower current income makes Section 179 less effective. If your business only shows $50,000 in taxable profit this year, taking a $300,000 Section 179 deduction is overkill. You can only deduct up to your net income. While the remainder can carry over, it complicates your tax strategy.

In a low-income year, bonus depreciation is often a better tool than either Section 179 or MACRS. Unlike Section 179, bonus depreciation has no taxable income cap – it can create a net operating loss that carries forward to offset taxes in future high-income years. If your accountant projects a low-income year followed by strong growth, the combination of bonus depreciation now and MACRS for the remaining basis may outperform both extremes.

Long-term planning favors gradual depreciation. If you just signed a massive five-year contract that will significantly boost your income starting next year, you will want tax deductions available during those high-income years.

Spreading deductions over time through a calculated equipment depreciation schedule ensures you have steady tax relief exactly when your business hits higher tax brackets. It provides predictable, reliable reductions in your tax liabilities year after year.

Common Mistakes When Using Equipment Tax Deductions

Navigating tax law requires precision. Many business owners make costly errors by misunderstanding how these rules apply to real-world operations.

Buying equipment only for tax reasons leads to bloated inventories and wasted capital. Never buy a $200,000 machine just to save $42,000 in taxes if your business does not actually need the machine. You are still spending $158,000 of real money. Only buy equipment that drives operational efficiency or revenue.

Misunderstanding eligibility causes audit nightmares. The equipment must be used for business purposes more than 50% of the time. If you buy a heavy-duty truck and use it mostly for personal travel, you disqualify yourself from these specific deductions.

Assuming federal deductions automatically reduce your state tax bill is a costly mistake. Many states, including California, New York, and New Jersey, do not conform to federal bonus depreciation rules and set their own lower Section 179 caps. A business in California claiming 100% bonus depreciation federally may still owe full state tax on that income, since California requires you to add the bonus depreciation back and depreciate the asset over its standard MACRS life at the state level. Always confirm your state’s rules with your tax advisor before projecting total savings.

Ignoring long-term impact hurts future cash flow. If you use Section 179 to deduct everything today, you will have zero depreciation deductions for this equipment next year. If your profits spike next year, you will face the full brunt of those taxes without the shield of ongoing depreciation.

Not aligning tax strategy with business needs creates friction. Consult with financial professionals and use resources from the US Small Business Administration to ensure your capital expenditures match your growth projections.

How Tax Strategy Affects Equipment Buying Decisions

Tax implications should directly influence how, when, and what you buy. Integrating tax planning into your procurement process completely changes your approach to equipment sourcing.

The timing of the purchase dictates everything. Tax benefits trigger in the year the equipment is placed into service. If you buy a combine harvester on December 28 but it does not arrive until January 3, the deduction moves to the following tax year. When sourcing globally, shipping times matter immensely. You must plan purchases months in advance to ensure delivery and deployment before the December 31 deadline.

New vs used equipment decisions become easier. Because Section 179 applies equally to both, you do not have to buy brand-new machinery to get the tax break. Buying a well-maintained, low-hour used John Deere tractor yields the exact same tax deduction parameters as buying a brand new one, but at a fraction of the initial purchase price.

Financing vs cash purchase strategies shift when taxes enter the chat. You might have the cash on hand to buy an excavator outright, but tax rules make financing incredibly attractive.

Financing vs Buying: Tax Implications You Should Know

You do not have to pay cash to claim a massive tax deduction. The IRS allows you to deduct the full purchase price of the equipment even if you finance it with a loan or specific types of leases.

Financing interacts beautifully with Section 179. When you take out an equipment loan, you receive the full machinery cost as a deduction in year one, but you only pay a fraction of that cost upfront in the form of a down payment and monthly installments.

The interest paid on your equipment loan is also deductible as an ordinary business expense, separate from and in addition to your Section 179 or bonus depreciation deduction. This makes financing even more tax-efficient than buying outright with cash, since a cash purchase eliminates the interest deduction entirely.

Equipment financing tax benefits create positive cash flow scenarios. Imagine financing a $250,000 machine with zero down and a first-year total payment of $40,000. If your Section 179 deduction on that $250,000 machine saves you $52,500 in actual taxes, your tax savings exceed your first-year loan payments. The equipment literally puts more cash into your pocket in year one than it takes out.

Lease vs purchase differences require careful attention. Capital leases or equipment finance agreements usually qualify for Section 179 because you are considered the owner of the equipment. True operating leases, where you simply rent the equipment and return it, do not qualify for Section 179, though you can write off the monthly lease payments as standard business expenses.

Always verify the structure of your loan to ensure you capture maximum equipment financing tax benefits.

How to Plan Equipment Purchases to Maximize Tax Benefits

Strategic procurement requires looking at the calendar, your balance sheet, and your operational needs simultaneously.

Planning purchases around tax year deadlines prevents missed opportunities. Start reviewing your fleet needs in Q3. Identify machinery that is aging out or new contracts that require specialized attachments. By sourcing in October or November, you allow ample time for global shipping, customs clearance, and delivery before the ball drops on New Year’s Eve.

Understanding business income projections dictates your deduction method. Work with your accounting team to project your year-end net income. If profits are surging, target Section 179. If profits are low but expected to rise next year, consider whether bonus depreciation – which carries no income cap and can generate a loss that carries forward – serves you better than MACRS alone. Work with your accountant to model which combination of bonus depreciation and MACRS best positions you for the high-income years ahead.

Aligning equipment needs with tax strategy ensures you never buy unnecessary iron. Create a priority list of machinery your business genuinely needs to scale. When your accountant gives you the green light that a heavy equipment tax deduction will highly benefit your current tax year, execute the purchase from that pre-approved operational priority list.

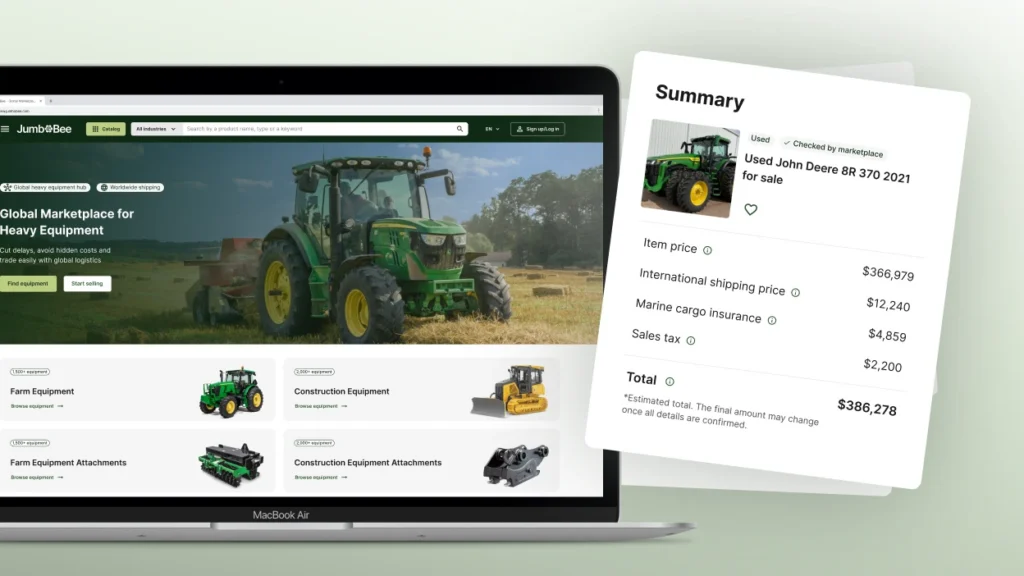

How JumboBee Helps You Optimize Equipment Purchasing

Executing a flawless tax strategy requires finding the right equipment at the right price, fast. Global equipment procurement used to be a logistical nightmare of hidden fees and shipping delays, which threatened year-end tax deadlines. JumboBee eliminates these hurdles.

Access global equipment options instantly. Whether you need a 2023 John Deere 9R 440 tractor or a 2018 John Deere 333G skid steer, our global marketplace connects you directly with verified sellers. You are not limited to local dealer inventory, allowing you to find the exact machinery that fits your budget and tax strategy.

Compare prices without hidden fees. JumboBee operates with complete transparency. You see the full cost instantly, including equipment, inspections, and shipping. This exact pricing allows your accounting team to calculate precise equipment financing tax benefits before you even click buy.

Avoid shipping delays that ruin tax deadlines. We handle all global logistics, customs, and import compliance. If you need a machine placed into service by December 31, our integrated shipping solutions ensure your equipment arrives ready to work.

Make cost-efficient decisions with optional professional inspections. Never risk your capital on unverified machinery. JumboBee facilitates independent inspections, so you know exactly what you are buying, ensuring your investment serves your business for years to come.

Explore equipment listings today. Compare global options, secure flexible financing, and find the right machinery to optimize your operations and your tax strategy.

Conclusion

Tax strategy drastically reduces real equipment cost. By leveraging government incentives, you turn massive capital expenditures into highly subsidized business investments. Understanding these rules is just as important as understanding the horsepower of the tractor you are buying.

Section 179, bonus depreciation, and MACRS each serve different purposes. Immediate expensing through Section 179 delivers maximum short-term relief in high-profit years. Bonus depreciation fills the gaps – with no income cap and no dollar ceiling, it is the most flexible tool for large purchases in any income environment. MACRS provides steady, predictable deductions for businesses, spreading tax relief across future high-income years.

The best choice depends entirely on the business situation. There is no universal right answer. Your corporate tax bracket, current net income, and future revenue projections dictate whether you should take the money now or spread it out over time.

Planning is key to maximizing benefits. Combine strategic tax planning with smart procurement. Utilize transparent global marketplaces to source high-quality machinery, leverage smart financing to protect your cash flow, and execute your purchases well before year-end deadlines to secure your deductions.

Be the first to leave a comment

There are no replies to this post yet. Share your thoughts and help start the conversation.